Unified Payments Interface : Payments is going through some radical shifts, as technology advances at a phenomenal pace. While the ecosystem moves forward with technology, UPI continues to be a catalyst for this transformation by redefining how we transact. What started as a regional phenomenon, National Payments Corporation of India’s Unified Payments Interface has emerged into an international playing field.

UPI is designed for ease of use, speed and security while facilitating multiple bank services on a single platform.

However, today a BA’s job is to do much more than simply study user journeys. To create competitive fintech products, BAs have to do go beyond surface-level transactions like ‘scan-and-pay’ and gain a deep functional understanding of the modern UPI ecosystem. This revised article explains the basics of UPI, its features and covers the deeper functionalities such as Credit on UPI, UPI Lite and Conversational Payments from a functional perspective.

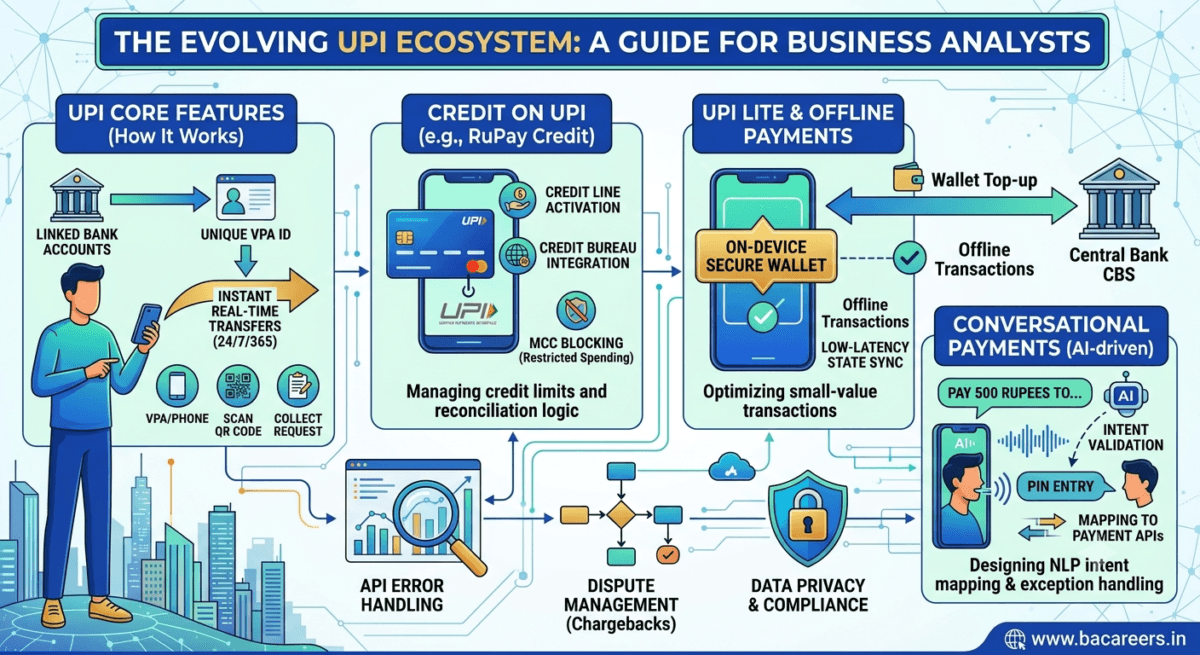

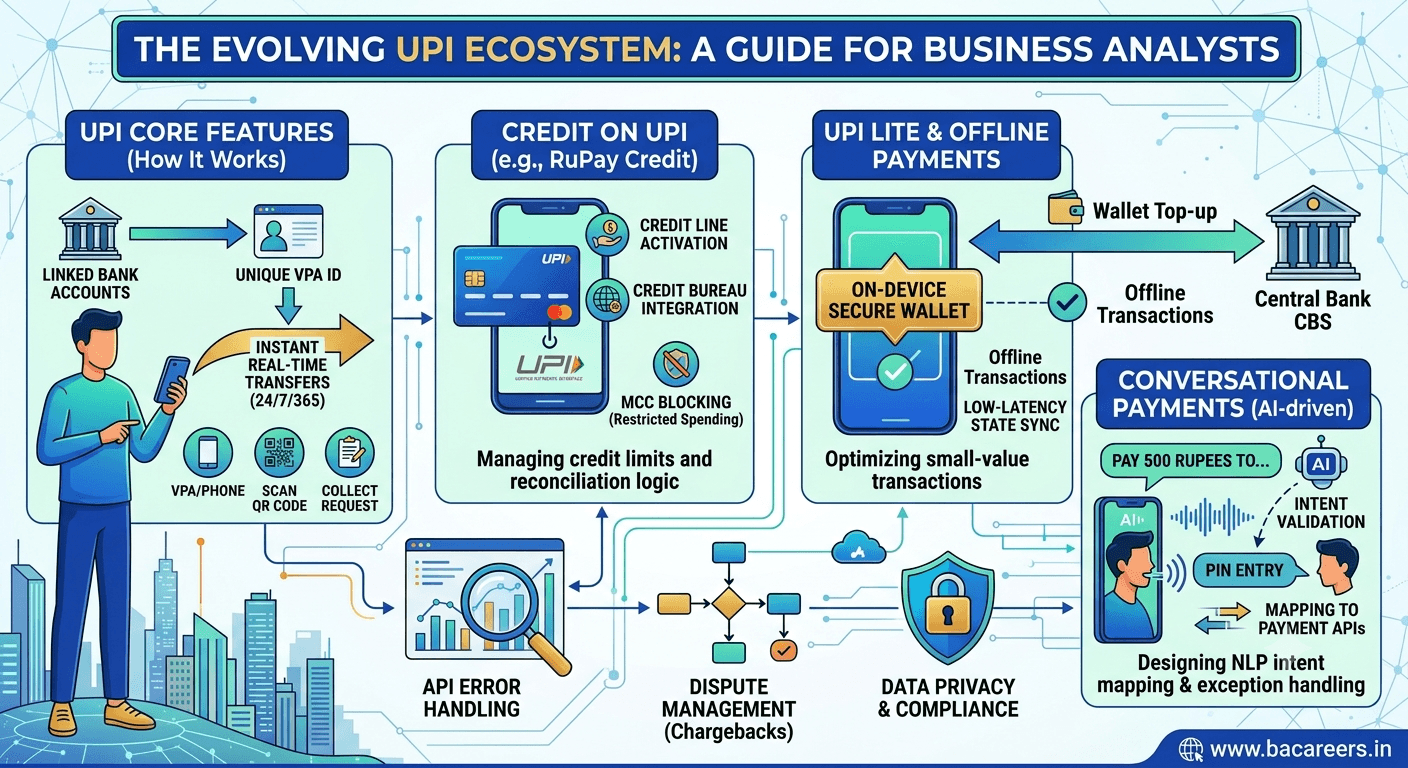

How UPI Works: The Core Features

The Unified Payments Interface comes with an extremely simple user interface that cleverly hides the complex payment clearing logic that exists at the back-end. When using UPI, a user links their bank account to a UPI-enabled app and creates a Virtual Payment Address (VPA).

This is their virtual financial address.

Transactions happen immediately via multiple interoperable methods:

- Initiating Payment via VPA / Mobile Number –P2P/P2M money transfer by sending funds through VPA. Sending an amount by using a UPI-enabled mobile number. Sending the money to yourself (transferring between your own linked bank accounts).

- Making a payment through dynamic QR codes – Dynamic codes generate with every transaction for merchant’s bill payment and can have expiry dates and specific values.

- Scan and Pay via QR codes (Static QR) – Using static QR code for P2P money transfer with no expiry.

- Send and Collect Requests –A sender can push a money request on to the payee, who can authorize the transaction.

Once the payee is ready, they will confirm the transaction, sending money to the payer from their account.

All transactions on UPI go through an authorization process via two-factor authentication. Transactions are processed by authenticating the transaction through a 4 digit UPI PIN of the remitter. Money movement takes place directly between bank accounts, 24/7/365.

The Modern UPI Ecosystem: Advanced Features for Business Analysts

As the UPI ecosystem continues to mature, NPCs introduce new technical architecture layers.

As a Business Analyst building user stories or managing product requirements for fintech products you will need to understand these three developing aspects of modern UPI.

1.Credit on UPI (RuPay & Credit Lines)

Traditional UPI transactions utilize direct debit from the customer’s account (savings). However, Credit on UPI is designed to offer services around credit risk management, zero interest periods, and also integrate with credit bureaus.

- The BA must design user journeys for the activation of bank credit lines, RuPay credit cards, and have a mechanism for tracking loan usage for customers.

- The BA must also be able to map unique merchant category code (MCC) blocking, credit card reconciliation with merchants and other such credit specific flows.

2. UPI Lite & On-Device

WalletsTo accommodate large number of high volume, low value transactions UPI Lite uses an on-device digital wallet on your phone. This means transactions don’t need to be routed to the bank’s core banking system (CBS) in real time and hence significantly reduces transaction failure rates across the network.

- As a BA writing functional requirements for a UPI Lite based feature, the key here is to build a state management layer that ensures the mobile app state and the central bank ledger state is synced at the back end.

Other technicalities to document include the limits around the on-device wallets, top-up and withdrawal processes and a resilient transaction mechanism that accounts for connectivity drops in the middle of a payment.

3. Conversational Payments (AI-Driven Flows)

UPI has begun to integrate with voice assistant technology that enables payments using voice command in different regional languages.

- For the BA building conversational payment features the task is to define language-based intent recognition flows.

- A BA must also identify key entity values within the language so that the conversation agent can create the necessary API call, but most importantly, without compromising the existing security controls such as UPI PIN for transaction authorization.

Functional Impact of UPI on Businesses

UPI’s widespread use has revolutionized the way businesses accept and make payments.

Many businesses benefit from accepting UPI as they don’t require costly POS hardware to process payments. E-commerce has also gained traction, as the quick and seamless checkout facilitated by UPI, significantly decreased the use of cash on delivery. It also serves as a foundational layer for P2P lending platforms, enabling the growth of split expense tools and other collaborative payment solutions.

Security, Regulations, and API Error Handling

UPI adheres to high-security standards outlined by the Reserve Bank of India (RBI) and is overseen by NPCI. End-to-end encryption and a strict, multi-factor authentication process with the secure UPI PIN are employed for every transaction. The most significant part of any UPI related technical analysis is the designing of exception handling workflows.

For example:Timeouts on Multi-Hop APIs -BAs must clearly define the transaction timeout for each step in the multi-hop UPI transaction for instance Payment Service Provider(PSP) application to the NPCI switch and from NPCI switch to the remitter bank and vice versa for beneficiary.

Dispute Management -The processes of handling dispute cases in a given time bound by following NPCI defined turn-around-time (TAT) protocol must be mapped by the BA.

Data Compliance – The requirements generated must comply with financial data privacy laws for the particular country, such as encryption and masking of sensitive user financial data.

Future Horizons & Emerging Technologies

UPI continues to expand beyond its domestic market, enabling cross-border transactions and partnerships with global payment networks in places such as Singapore, the UAE, Europe and more. The convergence of Payment with other innovative technologies such as Central Bank Digital Currencies (CBDC), blockchain for lower cost cross border transactions and biometric (fingerprint, facial scan) authentications is poised to usher in the next wave of payment innovation.

Conclusion

Unified Payments Interface (UPI) has already rewired the traditional method of money transactions and transformed legacy payment processes to something far more intuitive, fast, secure, and seamlessly interoperable.

For businesses, leveraging UPI will streamline financial transactions and increase reach, while for Business Analysts, deeply understanding its complex functional underpinnings will be crucial in developing industry-leading fintech products in the era of digital transformation.

Frequently Asked Questions:

Q1: How does Credit on UPI change the requirement gathering process?

A1: Credit on UPI introduces credit limit checks, credit bureau integration, and interest-period calculation logic into the transaction flow.

A Business Analyst must gather functional requirements for credit line activations, repayment alert systems, and merchant category code (MCC) blocking, which are entirely absent from standard debit-based UPI systems.

Q2: What is the primary role of a Business Analyst in UPI Lite development?

A2: The primary role involves creating the detailed state-synchronization logic between the user’s local mobile device storage (the on-device wallet) and the central banking servers. BAs must define precise validation rules for automated top-ups, daily transaction velocity limits, and clear reconciliation pathways for failed transactions.

Q3: How do BAs document conversational payment flows?

A3: BAs document these flows by designing functional conversation trees that map natural language inputs (user intents) directly to concrete payment API payloads.

The documentation must clearly handle exceptions like conversational ambiguity, payment re-prompts, and mandatory multi-factor authentication steps (like PIN validation) before processing.

Related Articles :

- BHIM UPI: The Future of Cashless Transactions in India

- UPI: The Future of Digital Payments

- Everything You Need to Know About UPI ID Meaning, Usage, and Security Measures

Business Analyst & Technical Content Writer specializing in Agile, Scrum, Requirements, User Stories, BRD/FRD, SEO blogs, and technical documentation.

{kind=link}

2 thoughts on “The Future of Payments: Exploring the Power of UPI” / “BHIM UPI”