Retail Banking Domain Knowledge: A Core Guide for Business Analysts

Retail Banking Domain Knowledge : Retail Banking Knowledge as a Central guide for Business Analysts. For any Business Analyst stepping into the finance services sector, merely understanding concepts such as deposits accounts and interest rates are not suffice. The modern banking landscape is cloud native and highly reliant on the concept of open data. In order to demonstrate the same level of technical knowledge as their peers in the FinTech realm, BAs in Retail Banking are expected to build a functionalbridge between legacy core banking systems (CBS) and new, customer facing fintech platforms. We are breaking down the core of these two systems into essential business and technical skills to learn for banking projects today:

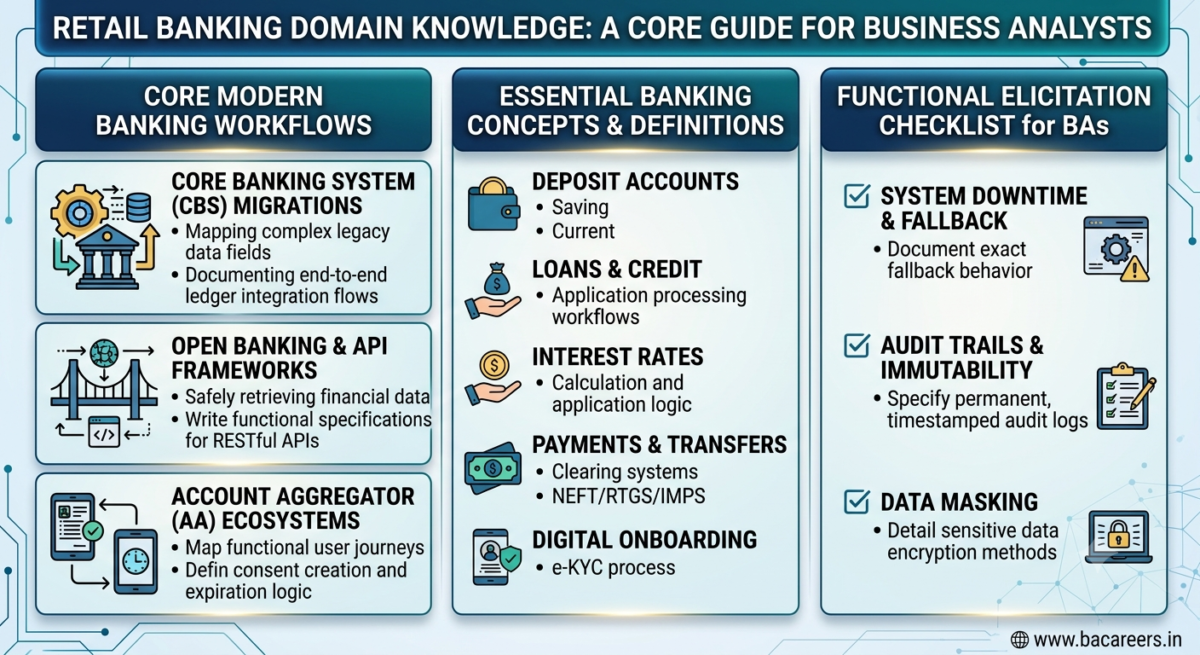

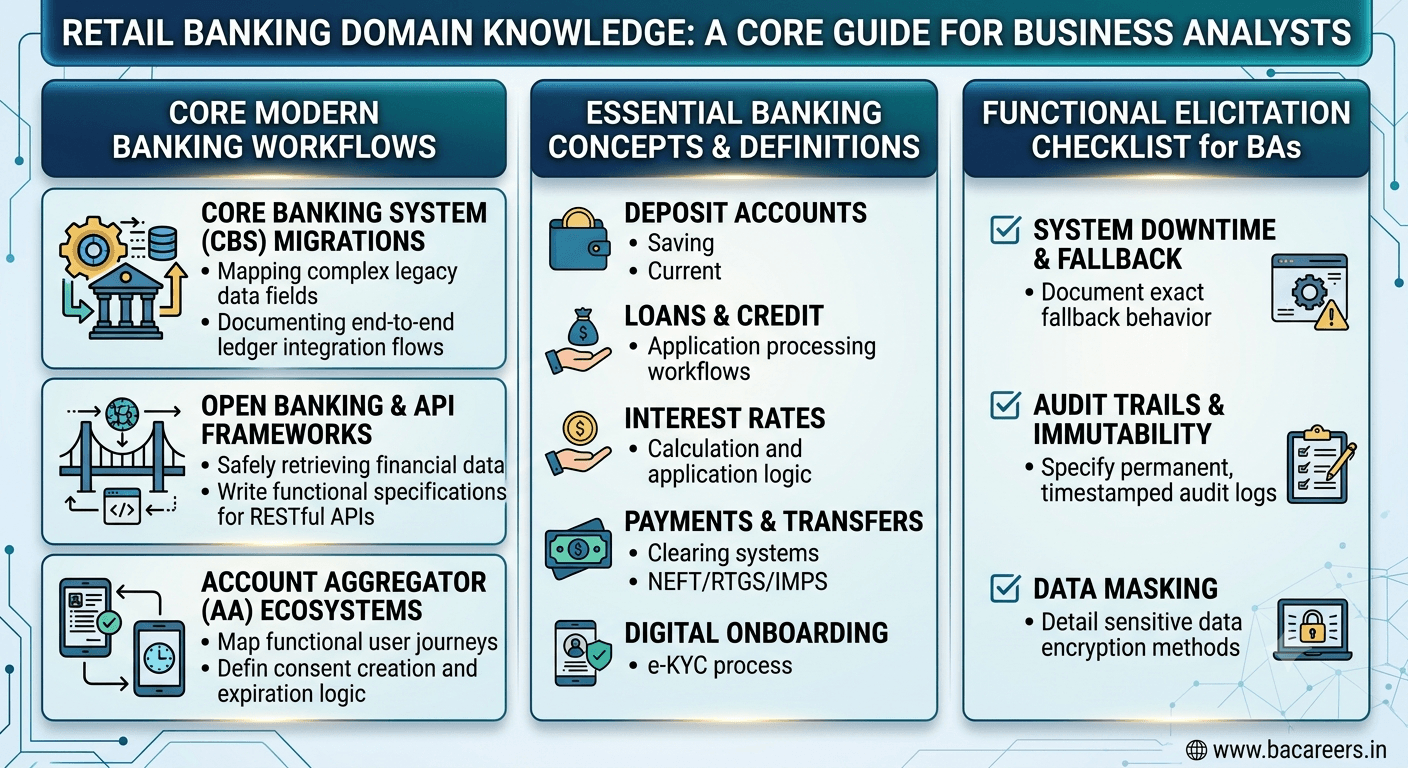

Core modern banking flows that a business analyst should know

For any Retail Banking project that you’re allocated to, your requirements gathering is usually centered around three architectural modernization changes:

- Core Banking System (CBS) Migration – Core Banking system is basically a backend database that contains all the ledger transactions, updates accounts, and balances on a daily basis. BA’s working on CBS migration need to be equipped with requirements for data field mapping of complex legacy data fields to new cloud systems,end to endledger integration process flows, and detailedrollbacklogic on transactions.

- Open banking & API framework – This refers to exposing all of your bank data through the use of REST APIs.

- This allows the third-party providers access to data like account balances,transaction histories etc in secure fashion.A Business analyst should know how to write functional specification for these APIs and detail data access controls to security, authentication etc.

- Account Aggregator (AA) ecosystem –AA system allows sharing of data from banks to third party providers via a consent-based framework. BA’s are expected to understand functional flows for creating these requests, system logic to enforce temporary digital signatures, and automatically expired consent timeline.

Checklist of functional requirements for retail banking

As you are drafting your FRD document or writing user stories, make sure to address these important points:

- System down time and rollback trigger – detailing what system behaviors are to be expected when a 3 rd party credit check bureau or automation tool goes offline mid transaction.

- Audit trail and immutability – specify to generate time-stamped and irreversible log records of all transactions to address compliance needs.

- Data masking – define in the requirements what information of the customer is to be masked in different UI screens and log outputs.

Retail Banking for Business Analysts Frequently Asked Questions (Q & A)

Q1:What is aCore Banking System (CBS)and why must aBusiness Analystunderstand it?

A: A Core Banking System (CBS) is a backend application that provides all core services such as account opening, deposit, loan account operations, customer data management, and transaction processing. As a Business Analyst working on retail banking, understanding CBS is crucial because any digital interaction a customer has with the bank, whether via a mobile app, website, or even an in-branch kiosk, ultimately interacts with this central system to retrieve and update customer data and transactions.

A BA must ensure that any new feature is seamlessly integrated and doesn’t cause any disruption or sync errors with the CBS.

Q2:How doAccount Aggregator (AA)ecosystemschange thedesignapproach ofaBusinessAnalyst?

A: Account Aggregators (AAs) revolutionize design by shifting the focus from manual document submissions (like uploading PDFs) to digital, consent-driven data sharing via APIs.

BAs now need to design user journeys around how customers grant, manage, and revoke consent for their financial data to be accessed by Financial Information Providers (FIPs).

This requires detailing the functional flows for consent creation, managing secure, temporary digital signatures, and defining the rules for automatic expiration of consent, emphasizing a much more secure, real-time, and user-centric approach to data sharing.

Q3:WhatcomplianceframeworksshouldaRetail Banking BAbeawareof?

A: A Retail Banking BA must be well-versed in local and international financial regulations such as KYC (Know Your Customer),AML (Anti-Money Laundering), data sovereignty laws (e.g., GDPR if operating in certain regions), data privacy regulations, and secure authentication standards. Familiarity with these frameworks is essential for ensuring that the designed solutions meet security requirements, pass internal and external audits, and maintain customer trust.

Related Articles :

- Domain Knowledge for Business Analysts: Why It Matters & How to Gain It

- The Future of Payments: Exploring the Power of UPI” / “BHIM UPI

- Payments Business Analyst: Job Description, Skills & Career Path (2026)

Business Analyst & Technical Content Writer specializing in Agile, Scrum, Requirements, User Stories, BRD/FRD, SEO blogs, and technical documentation.

{kind=link}